TO RECEIVE THE LATEST NEWS FROM WE THE GOVERNED DELIVERED STRAIGHT TO YOUR INBOX –SUBSCRIBE HERE

SUPPORT WE THE GOVERNED – MAKE A DONATION HERE

Forterra, previously known as the Cascade Land Conservancy was founded as the Seattle/King County Land Trust in 1989 in Washington State. This non-profit was originally focused in the Seattle and King County areas, but has expanded to include land acquisitions and transactions from Yakima County in Central Washington to the Pacific Coast of Washington State. Many observers liken the organization to a local version of the Nature Conservancy.

The Forterra website and Public Relations campaign portrays itself as an organization purely focused on the environment with a nice mix of political socially conscious intersectionality buzzwords tossed into the mix. Forterra’s ties to political leadership in Washington runs deep and their fundraisers are well attended by the political insider class in the King County/Seattle area. However, a recent lawsuit in King County Superior Court has drawn some needed attention to a common problem uncovered with many “non-profit” land conservancy organizations like Forterra around the nation. Few people bother to look at the intersection of these many land transactions and political insider personal benefits like questionable tax deductions for donors, and the use of public funds to profit a “non-profit” organization which also has many for-profit elements. Let’s consider tax fraud first.

The lawsuit (original complaint linked here, and preliminary injunction linked here) involves a 27 acre piece of commercial property located in Kent near Hwy 167 and 212th street. This property apparently has some serious problems. Documented landslides, covered in wetlands (and buffers), evidence of homeless/drug addict camps, and other challenges greatly reduce whatever perceived value this property might normally have as raw land. The lawsuit mostly involves complaints by the plaintiffs against Forterra apparently for negligent misrepresentation and attempting to deceive the buyer about the many problems and deficiencies of this property. Part of this case appears to show Forterra denying knowledge about property deficiencies which they had only recently discussed with the City of Kent (and which were public records). This article won’t address those claims, but they appear to be well laid out in the original complaint (linked here) and the attached exhibits (linked here and here). While there appears to be a variety of motion practice in this lawsuit over the past few months, Forterra has yet to formally respond to the complaint, but they give some hints about their side of the case in filings they have made (linked here , here, and here).

While King County Superior Court will be the venue for exposing or refuting the claims of fraud against Forterra, the attention to this piece of property raises questions I’ve had for many years about some of the questionable land transactions in which organizations like Forterra have engaged over the past few decades. Let’s look at the concerns about tax fraud.

Forterra’s inspiration – The Nature Conservancy – A history of Corruption

Nature Conservancy, which is a massive, international mega corporation which has also presented itself as a land conservancy for decades, has found itself in hot water on numerous occasions for a variety of scandals. Forterra and other similar organizations like this in Washington State were inspired by and appear to have most closely modelled their organizations to be similar to Nature Conservancy. The Washington Post ran a series of articles in 2003 and 2004 detailing the plethora of scandals documented at the Nature Conservancy at the time. It is also worth noting that the Nature Conservancy is currently active in Washington State politics, most notably, their recent cash contributions of $3.25 million and donation of $448,477 of “staff services” to support the most recent failed carbon tax initiative I-1631 (see this spreadsheet which details all reported $3,776,254 of political contributions made by Nature Conservancy in Washingont State in the last few years). From the Washington Post in 2003:

“While the Conservancy has done much to preserve green spaces, its strategy of combining conservation and business, including its own pursuit of for-profit ventures, has led to some costly misadventures and awkward positions:

- The drilling foray, on the Texas Gulf Coast, turned into a fiasco. Not only did some endangered birds die after the Conservancy started drilling, but the charity also sold natural gas owned by someone else and kept the profits. The Conservancy and its partners settled a resulting lawsuit last year for $10 million.

- In Virginia, the Conservancy has invested in a number of for-profit businesses on the Eastern Shore: a bed-and-breakfast, an oyster-and-clam farm, an “heirloom” sweet-potato-chip operation, a seaside home development. The businesses failed, leaving a $24 million debt.

- The Conservancy has profited by selling its name and logo to companies, which use the image to gain what one corporate executive calls “reputational value.” A Conservancy focus group study found that a few participants said accepting corporate cash in certain cases would be “the equivalent of a payoff.”

- The charity engages in numerous financial transactions with members of the Conservancy family — governing board members and their companies, state and regional trustees, longtime supporters. The nonprofit organization has bought land and services from board members’ companies, and it has declined to release property appraisals from the deals. It has sold choice Conservancy land to past and present trustees through its “conservation buyers” program, which offers steep discounts in exchange for development restrictions. It has lent cash to its executives, including $1.55 million to its president.

- The Conservancy’s mission makes it reluctant to take positions on some leading environmental issues, including global warming and drilling in Alaska’s Arctic National Wildlife Refuge. Corporations represented on the Conservancy’s board and advisory council have lobbied nationally on the corporate side of the issues. A Conservancy official said the group avoids criticizing the environmental records of its corporate board members.

- Some of the charity’s scientists have complained that the organization has drifted from its stated commitment to the “best available science.” One scientist complained in an internal 2001 Conservancy study: “Science is not understood or supported by senior managers and state directors. [The] entire focus is on land deals.” Said another: “I am not convinced [the Conservancy] is science-based, as we claim.”

– Washington Post – May 4, 2003 (linked here)

When the Nature Conservancy took some donated land in Texas to protect a local endangered species (the Attwater’s prairie chicken) and started drilling oil on that land, they were not very good stewards of the land (see article here). In addition, they became embroiled in a lawsuit for stealing mineral rights and attempting to defraud another non-profit at the same time. Board members of the Nature Conservancy were accused of attempting to engage in a fraudulent scheme to acquire these mineral rights under false pretenses from the Sage Foundation.

The Nature Conservancy was also exposed for paying premium prices for valuable land and then selling that same land to Nature Conservancy employees and insiders (see story here), plus making sweetheart home loans to insiders (see story here). The Nature Conservancy claimed their finances were an “open book” but were actually very deceptive about the true nature of their finances (see story here). Like Forterra, the Nature Conservancy also was very focused on ensuring they maintained a positive public image and were willing to spend significant resources to create and craft this image (see story here). The Nature Conservancy responded to these articles (see article here). However, ultimately, an IRS investigation into a variety of questionable Nature Conservancy activities (see story here).

More recently, the concerns about Nature Conservancy’s mismanagment of their lands and misuse of the cash (often public funding) continues to lead to litigation (see 2018 press release linked here, and article linked here regarding a Califoria case of mismanagement). in 2017 the Brookings Institute published a report on the problems of “Conservation Easements” (see report here), which are often marketed by Land Trusts and similar organizations as a way to “conserve the land.” However, as this report states about these conservation easements:

“A tax deduction intended to encourage conservation of environmentally important land and historic buildings has become a lucrative way for real estate developers to finance development projects—reducing their tax payments by billions of dollars, and in some cases doing little to advance environmental protection.”

Brookings Institute, May 2017 – “Charitable Contributions of Conservation Easements”

Due to the tax fraud problems associated with these “conservation easements” and other similar issues, the IRS has taken some strong steps to change tax policy related to these programs (see here and here). Forbes also ran an article about the abuse of this process by high net worth individuals and “non-profits” (see article linked here). This background on the Nature Conservancy, which is one of the biggest organizations of its kind in the world and on which local land grant “environmental” organizations like Forterra were modelled and inspired, is helpful to put serious concerns about Forterra in a national context.

Pump up phony value for maximum tax deductions for donors (if they donate additional cash)

The recent lawsuit against Forterra in King County involves a 27-acre parcel which was donated to Forterra in 2008 by a company named Kent Sidehill LLC (See donation document referenced here). The main principal of this organization is Alan Black (See Secretary of State incorporation document here), who signed the final Warranty Deed (linked here). The property was valued, for purposes of this donation, at $880,000 (See WA Dept. of Revenue signed REET linked here). However, in both later appraisals done in more favorable real estate markets (see 2016 appraisal of this property for $320,000 linked here, page 9) and according to the King County Assessor’s office records, this property has never been within $500,000 of this claimed “value.” At the time of the donation during one of the worst real estate markets in recent history, this inflated value was justified with an appraisal commissioned by the owner of the property at the time for purposes of “donation to a charitable organization” (p.17). See this 2008 “appraisal” linked here.

Inflated values of property donated to charities allows the donor to take tax write offs which can be financially beneficial to the donor. The receiving charity has every incentive to cooperate (and even assist) with these inflated values because it helps create more incentive for the land donation in the first place. Ultimately, this type of donation/land transaction creates little incentive for either party to correctly represent the value of the donation since both parties benefit from an inflated transaction value. In fact, the only “loser” is the IRS, since the owner would have been able to write off what was probably an exaggerated value of $500,000 +/- of land value as a “donation” to the “non-profit” Forterra.

Interestingly, according to Forerra’s own public records, the principal owner of this property, Alan Black, was also a listed cash donor to the organization (see 2010 annual report linked here – page 17). Also, note, according to this 2011 email (linked here), this donor created a planned Forterra cash donation schedule upon completion of the land “donation” to Forterra. Note, the total cash donations defined in this email were $25,000 – $39,000 (depending on some implied conditions), which still allows the donor to both profit from dumping a challenging and encumbered piece of property and take a major tax deduction from the donation, in excess of the aditional cash donation to the “non-profit” piece of the Forterra corporate structure. Other interesting emails about this property can be found here and here. Forterra profits by taking the property, then profits again via taxpayer dollars when they unload the property to a city, county, state or other government entity. To keep the skids greased, they convince the lucky land owner/donor to kick in some cash as well.

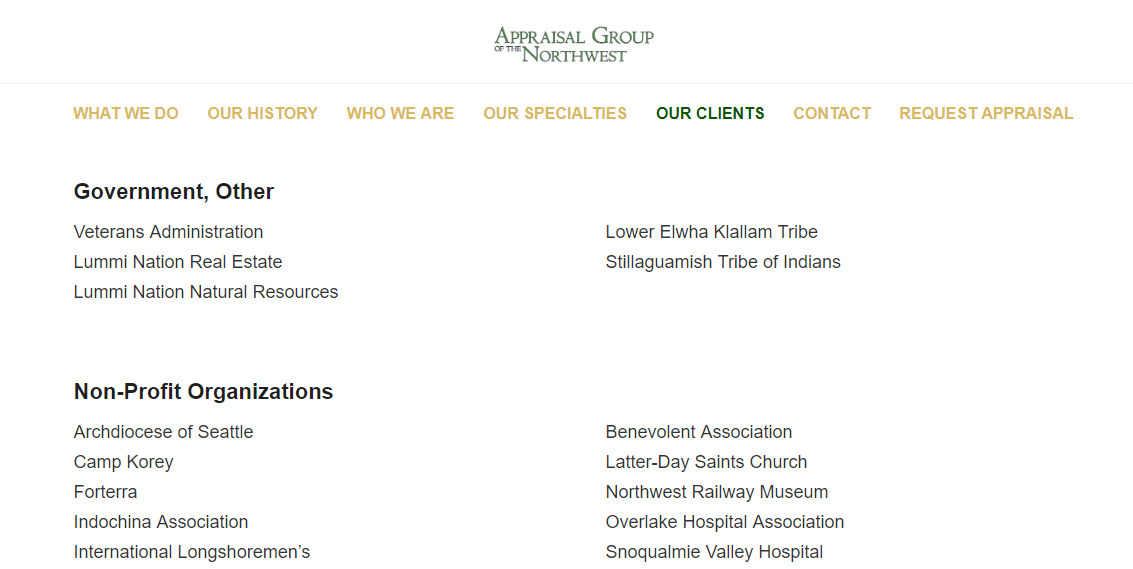

One note of interest here is the appraisal company used by the original property owner lists Forterra as one of its major clients on its website (linked here, and screen captured here – in case it is changed in the future). The appraisal company listed the Cascade Land Conservancy (Forterra’s old name) as one of its main customers in the original appraisal document from 2008 (see page 54), so this affiliation was predating this transaction and continued afterwards. This creates a likely conflict of interest when the appraisal company inflates the value of this property.

Tax fraud is not an uncommon concern around land trusts and similar organizations. As the stories about Nature Conservancy help document, there are all types of ways for political insiders and wealthy donors to game the system and use organizations like this to defraud the Federal government of taxes or to just personally profit themselves. Rumors about these types of transactions have swirled around Forterra (and when they were called the Cascade Land Conservancy) for years, but few people are willing to spend the time or energy to take a closer look. Perhaps now it is worth looking a bit closer at Forterra and some of their reputed “400 land transactions” over the past few decades to see just how common this type of activity may be.

Land trusts, public purchases, litigation, and conflicted judges

Forterra, just like the Nature Conservancy, and just like many similar land trust type organizations are structured to benefit from close ties to political insiders. For example, Dow Constantine is the Executive Director of King County and is listed by Forterra as being on their board. Tukwila City Councilman D’Sean Quinn is also listed on this board (I wrote about Quinn in an earlier article when he failed to disclose his affiliation with Forterra in his personal financial affairs forms filed with the Public Disclosure Commission here and was also voting to approve grants to Forterra). Also, former Mercer Island Deputy Mayor and long time councilman (recently retired) Dan Grausz is involved. Many noted political and bureaucratic insiders are formally associated with Forterra.

These close ties to political insiders are relevant when the organization conducts as much business as Forterra does with land purchases, swaps, zoning, and regulations. In this 27 acre parcel of land referenced in the lawsuit complaint, Forterra clearly had plans to convince the City of Kent to purchase it from Forterra at a pretty high price. Kent used a real independent appraisal company and determined that it was not in Kent’s best interest to do so, which is partly what appears to have led to this lawsuit. According to the Plaintiff in this case, Forterra attempted to conceal the many problems with this property identified by Kent in their due diligence phase earlier from this latest prospective buyer. This attempted concealment, if true, was not wise because these documents would have been a public record at the City of Kent, and the plaintiff appears to have acquired them through public records requests. Of note, here is a short list of other parcels Forterra appears to currently own and their expectations for profit by transferring ownership of these lands to various public entities (see Forterra 2016 spreadsheet project list linked here for reference).

Whether Forterra is found to have committed fraud or not in this instance, the plaintiffs have a difficult path at least in part due to the judge they were assigned in this case. Judge Douglass North is not a disinterested adjudicator in this matter, considering his previous articles and stances before he was appointed to the King County Superior Court in 2000 to fill a judge retirement. For example, he was the former “Conservation Chair” of the Northwest Rivers Council of Seattle and a founding board member of the Rivers Network. He wrote articles titled “Countering the Resource Abuse Movement” (see p.4 linked here), which he defined anyone who disagreed with his policy prescriptions as “abusers.”

North also Like most judges, he was recently “reelected” with no opposition in 2016. He did have a primary in 2012, was endorsed by the Seattle Times (see here), but was elected with 60% of the vote. While not the main point of this article, judges with this type of clear bias and background should not be assigned cases like this. Interestingly this judge has also been disciplined by the state judicial ethics board in the past (see final stipulation here), and he had to take additional judicial ethics training (see proof of attendance here).

Is Forterra structured to encourage and facilitate tax fraud? The evidence surrounding the inflated value for this piece of land certainly supports this contention, but to determine a full and consistent pattern of behavior, it would be most effective to review some of these 400 transactions that have been made by Forterra in Washington State over the past few years. One challenge with this process is the fact that Forterra has created a web of for-profit and “non-profit” ventures that are all intertwined in a manner designed to make sorting out the facts more difficult without a deep discovery dive in litigation or insiders willing to spill the beans (see this document for one of their recent corporate structure diagrams on page22).

This article is likely to be a Part I, and I’d encourage others with insider knowledge to contact me and forward the information they might have about this or other transactions which either support or refute this contention. With such close affiliation with so many local politicians, political insiders, and senior level bureaucrats, this type of organization is well-positioned to profit from this political influence, and judging from the many concerns exposed by the Nature Conservancy controversies, it would be prudent to dig deep and look even closer. Millions of our taxpayer dollars are used to ensure this “non-profit” gets plenty of cash profit, and as taxpayers we deserve to know the truth.

OUR CONSTITUTION BEGINS WITH THE PHRASE “WE THE PEOPLE.” IT WAS THE FOUNDER’S INTENT THAT GOVERNMENT BE CREATED BY THE PEOPLE, TO SERVE THE PEOPLE. IT WASN’T THEIR INTENTION FOR THE PEOPLE TO SERVE THE GOVERNMENT. IT WAS ALWAYS INTENDED THAT GOVERNMENT WHICH FAILED TO SERVE THE PEOPLE SHOULD BE “ALTERED OR ABOLISHED.” UNTIL WE RETURN TO THE FOUNDER’S INTENT, WE REMAIN WE THE GOVERNED…

Background articles and documents:

Forterra Background:

Seattle Times – 2011 – “Cascade Land Conservancy is now Forterra”

Cascade Land Conservancy 2010 Annual Report (now Forterra)

Tukwila Ethics Board Hids Forterra Grant Funding Violations

2008 appraisal of Kent Sidehill property donation by Forterra vendor – $880,000 value (note p.17 intended use as “donation”, p.54 Cascade Land Conservancy has been client of appraiser)

Kent Sidehill, LLC – Sec. of State business information

Forterra – 2016 Project List Draft Spreadsheet

Recorded Warranty Deed for Kent Sidehill property to Cascade Land Conservancy in 2008

Signed Dept. of Revenue REET document stating value of property at $880,000

Signed Dept of Revnue REET affidavit for kent Sidehill property donation to Cascade Land Conservancy

Nature Conservancy Background

Washington Post – Jan. 17, 2004 – “IRS to audit Nature Conservancy from Inside”

New York Times – Aug 3, 2014 – “Group earns oil income despite pledge on drilling”

Washington Examiner – Jan 10, 2013 – “Nature Conservancy embroiled in another land grab scandal”

IRS – Background – Abusive Transactions Involving Charitable Contributions of Easements

IRS – Conservation Easement Audit Techniques Guide

Washington Post – May 4, 2003 – “Nonprofit Land Bank Amasses Millions”

Washington Post – May 4, 2003 – “Image is a Sensitive Issue” (article about Nature Conservancy focus on PR

Washington Post – May 6, 2003 – “Nonprofit sells scenic acreage to allies at a loss”

Washington Post – May 5, 2003 – “How a bid to save a species came to grief”

Washington Post – June 13, 2003 – “12 Home Loans at Conservancy”

Washington Post – May 16, 2003 – “Charity hiring lawyers to prevent Hill probe”

Washington Post – May 13, 2003 – “Nature Conservancy Suspends Land Sales”

Washington Post – June 8, 2005 – “Senators Question Conservancy’s Practices”

Washington Post – May 4, 2003 – “$420,000 a year and no strings fund”

IRS shines a spotlight on syndicated conservation easements

Washington Post – May 5, 2003 – “On Eastern Shore, For-Profit ‘Flagship’ Hits Shoals”

Washington Post – May 13, 2003 – “Balancing the Nature Conservancy Story”

Brookings Institute Report- November 2017 – “Charitable Contributions of Conservation Easements”

Forbes – July 24, 2017 “New IRS Scandal – Syndication Of Conservation Easement Deductions”

Background on Forterra Fraud Lawsuit

Case #18-2-55191-9 SEA – S. 212th Street LLC vs. Forterra – complaint

Case #18-2-55191-9 SEA – Plaintiffs Motion for Preliminary Injunction

Case #18-2-55191-9 SEA – Plaintiffs Declaration

Case #18-2-55191-9 SEA Plaintiffs Exhibits A-Y

Case #18-2-55191-9 SEA Forterra Response to Motion for Contempt

Case #18-2-55191-9 SEA Declaration of Forterra’s Daniel Grausz

Case #18-2-55191-9 SEA Declaration of Forterra’s Michelle Conner

Nature Conservancy Political Donations:

Background on King County Superior Court Judge Douglass A. North

Judge Douglass North official Bio on King County website. If this link is disabled, here is the bio downloaded from their site – linked here.

Bar Bulletin article about Judge North’s Ethics Board Conduct Report

STIPULATION, AGREEMENT AND ORDER OF ADMONISHMENT for Judge Douglass A. North- December 8, 2017 – Case # CJC No. 8583-F-174 . If this link is disabled, a downloadable copy is available – linked here. Also, here is the certificate (dated May 11, 2018) that says he completed his additional judicial ethics training class.

Douglass North article “Countering the Resource Abuse Movement” page 4 – June, 1992 – North claims to be the voice of the River.

Douglass North has authored a handful of Whitewater Kayaking books

{kind=link}